Reveal

Potential

Reach the heights of trading with us! We offer a wide range of trading accounts suitable for traders of all levels.

Get Started

First steps

How to Start Earning

1step

Think

Consider several ways to earn money on the exchange. Assess their advantages and disadvantages. Choose among them the most suitable for you.

2step

Choose

Find several tools on our platform for investing and choose among them the most suitable one. Register and open a minimum deposit.

3step

Earn and Learn

Try different approaches, learn from your actions, gain experience. Analyze your steps, work on your mistakes, improve your skills and strategies.

Features

Open a World of New Financial Opportunities

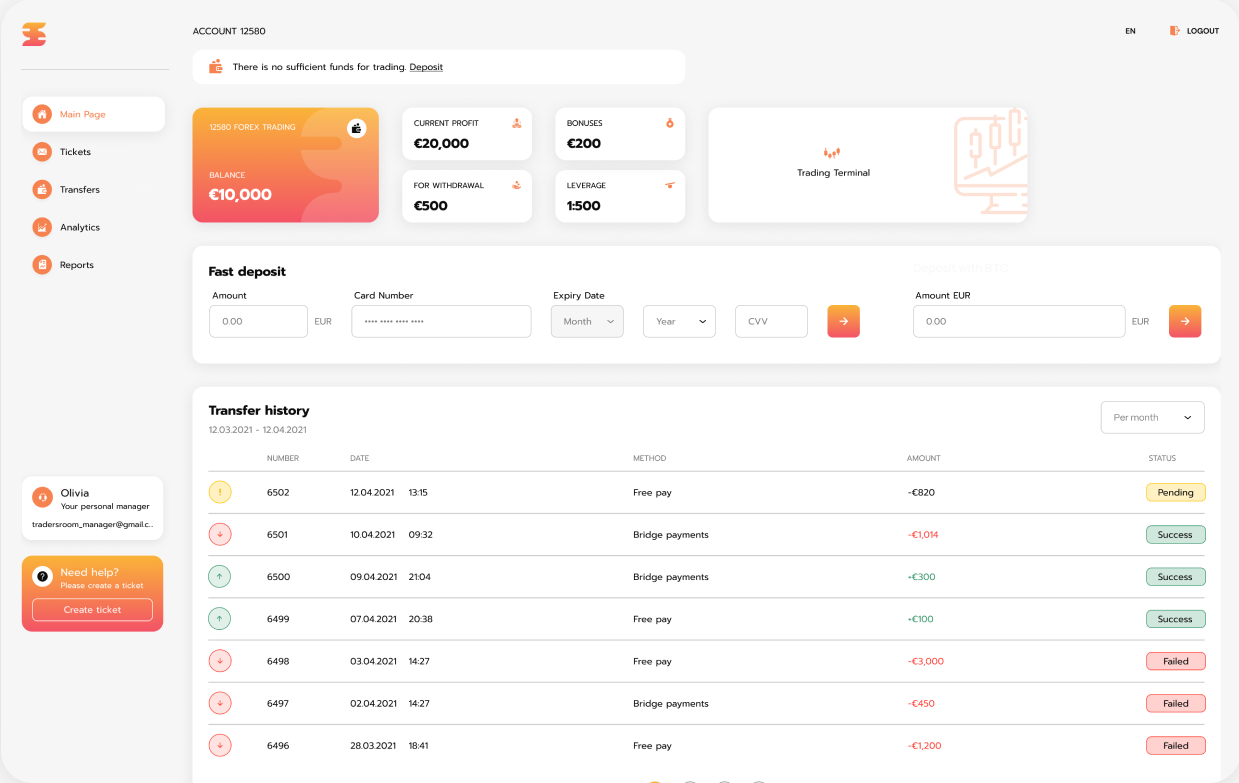

Investments

Explore a wide range of trading instruments, carefully selected for their high liquidity, allowing you to make optimal investment decisions.

Analytics

Gain access to exclusive market research empowering you to learn how to predict chart movements alongside our team of traders.

VIP Club

Join an international community of traders and unlock privileges that are typically unavailable to the majority of market participants.

Safety

The real-time margin calculation system reflects the market revaluation of all client positions, ensuring an accurate risk.

Explore a variety of options and trade with confidence, taking advantage of global market trends and making informed investment decisions.

Custom reports

Personalized Reports Customized for Your Needs

Every trader has unique requirements for analyzing and monitoring their trading activity. That's why our company provides customized reports specifically tailored to each client's needs. Our team of professionals works closely with traders to create personalized reports that highlight performance metrics, market analysis or visualization of specific data.

Personalized support

Comprehensive Support Service for Every Trader

Our company prioritizes effective communication with clients, providing a professional support service to address all financial inquiries related to trading. Our team of experts is always available to assist with any questions and ensure seamless trading experiences.

News

Stay Up to Date With the Trends and Happenings

12.06.2026

Futu founder Leaf Li accelerates global expansion after $273M penalty

Futu Holdings' Global Ambitions amid Regulatory Challenges

China's securities regulator has targeted Futu Holdings with a substantial fine for unlicensed trading activities. Yet, what might seem like a significant setback is part of a pre-existing strategic pivot by the company towards international markets. This ambitious strategy aims to dilute reliance on Futu's home market and reduce exposure to China's stringent regulatory environment, showcasing the foresight of founder Leaf Hua Li.

The Regulatory Clampdown

On May 22, the China Securities Regulatory Commission (CSRC), along with its Shenzhen bureau, proposed a hefty administrative penalty amounting to around $271-$273 million. These charges stem from allegations that Futu was engaging in unlicensed securities and futures business activities targeting clients from mainland China. Additionally, Leaf Hua Li, the company's founder, was hit with a personal fine of RMB 1.25 million. This significant blow, however, is being met with a robust international strategy which was already in progress.

Navigating Through Numbers

Futu's strategic pivot is reinforced by compelling financial data. Today, mainland Chinese clients constitute a mere 13% of the company's total funded accounts. Conversely, international clients, served primarily through the Moomoo brand, now represent over 55% of Futu's client base. The company’s Q1 2026 financial metrics emphasize growth and resilience despite regulatory scrutiny. With a substantial revenue of $746.9 million, marking a 25% increase year-over-year, and a remarkable rise in total client assets to $155.8 billion, the company is clearly reaping the benefits of its international expansion.

Expansion into Cryptocurrency

Futu's global expansion strategy isn’t confined to traditional securities. In a world growing increasingly digital, Futu has ventured into the realm of cryptocurrencies. Through its PantherTrade platform, the company is pioneering licensed virtual asset trading in Hong Kong, offering an innovative blend of cryptocurrency trading services combined with integrated securities financing options. This diversification aligns with global investment trends and sets Futu apart in a competitive financial landscape.

Market Dynamics and Investor Considerations

Unsurprisingly, Futu's stock experienced a tumultuous period following the penalty announcement, with variations ranging between an 8% and 37% drop. Similarly, Li's personal net worth witnessed a decline from its previous estimation of around $7.6 billion. Yet, when placed in broader financial context, the penalty equates to about a third of a single quarter's revenue. Given the company's robust financial health, represented by $155.8 billion in client assets, the penalty is a significant but not fatal blow.

Implications for the Broader Fintech Sector

Futu's experiences are a cautionary tale for other Chinese fintech companies operating in the realm of cross-border financial services. The CSRC’s stringent measures underscore a broader regulatory tendency towards heightened scrutiny on businesses that blur the line between domestic and international markets. As Futu demonstrates, strategic diversification and international market engagement could be both a buffer and a growth pathway for companies operating under similar pressures.

Conclusion: The Road Ahead for Futu Holdings

Futu Holdings stands as a compelling case study in turning regulatory challenges into opportunities for strategic expansion. Through diversification into international markets and innovative sectors like cryptocurrency, the company is not merely surviving but thriving. As the financial climate continues to evolve, Futu's experience offers valuable insights for other businesses navigating similar landscapes. Future vigilance and adaptability remain paramount as companies like Futu forge paths toward sustainable growth and global financial success.

10.06.2026

AI, digital assets and the end of legacy compliance

The Transformation of Compliance in Global Banking

Compliance has transitioned from a peripheral function within the back office to a central component in the boardroom strategy for global banks. It has evolved from a quiet operational component to a dynamic and influential element that shapes how financial institutions handle growth, adopt new technologies, regulate employee behavior, and meet increasing regulatory demands across various jurisdictions. This marked shift indicates the escalating importance of compliance in the modern banking sector and its impact on the overall strategic operations of banks.

Navigating the Complex Landscape of Global Risk and Regulation

According to insights from StarCompliance, the challenge facing global banks goes beyond the sheer volume of regulations. The entire operating landscape has become more interwoven, causing traditional compliance risk management structures to lag behind. StarCompliance recently highlighted three critical areas: global risk, the governance of artificial intelligence (AI), and regulatory pressure.

Financial institutions are currently managing several simultaneous challenges, including expectations surrounding AI governance, oversight of digital assets, meeting operational resilience requirements, enforcing sanctions, adjusting to evolving accountability frameworks, and navigating an intricate tapestry of regional regulations. The convergence of these pressures, arriving simultaneously rather than sequentially, presents diverse supervisory expectations unique to each market, creating an acute situation for banks to address.

The Challenge for Compliance Teams in Fostering Innovation

For compliance teams, this climate poses an ongoing balancing act. They are tasked with enabling innovation and facilitating business growth while demonstrating effective governance, maintaining defensible oversight, and achieving real-time risk visibility across the organization. These objectives must be met amid increasing complexity and regulatory scrutiny.

Transitioning from Traditional Compliance Models

Traditionally, many banking compliance programs were designed for more centralized and predictable regulatory environments. However, that model is now under strain. Financial institutions are processing larger data volumes, managing employee activities across numerous markets and digital platforms, and facing increasingly intricate reporting obligations. Simultaneously, regulators are emphasizing active demonstration of compliance controls versus merely having policies exist on paper.

This shift compels banks to fundamentally reassess their compliance infrastructure. Disconnected systems, fragmented reporting, and manual oversight processes introduce operational delays and leave institutions vulnerable when regulators request evidence, escalation histories, or audit trails at short notice. Consequently, compliance technology, governance, and data management are being reconsidered at an enterprise level.

The Role of Artificial Intelligence in Compliance

Artificial intelligence is accelerating this transition. Banks are increasingly exploring AI-driven surveillance, monitoring, and risk detection tools. However, this comes with heightened scrutiny from regulators regarding governance, accountability, explainability, and model oversight. For compliance leaders, the focus has shifted from debating AI deployment to determining responsible usage within existing regulatory frameworks.

Expanding the Risk Perimeter with Digital Assets and Employee Conduct

The intersection of traditional finance and digital assets represents another significant shift. Activities like cryptocurrency trading, tokenized assets, decentralized finance platforms, and prediction markets introduce new risks concerning employee conduct and information that existing surveillance programs were not originally designed to capture.

This is especially critical for global financial institutions, where escalating regulatory focus is on conflicts of interest, material non-public information, and employee trading activities that extend beyond traditional brokerage accounts. Compliance programs require visibility across more financial activities, necessitating technology that can adapt to evolving market structures.

Adapting to a Connected Compliance Approach

As regulatory complexity intensifies, many banks are gravitating towards more centralized and connected compliance operating models. The emphasis is shifting towards integrating governance, surveillance, employee disclosures, case management, reporting, and audit documentation into cohesive frameworks that can scale globally while accommodating regional regulatory demands.

StarCompliance has positioned itself at the forefront of this shift. For over 25 years, StarCompliance has collaborated with financial institutions worldwide to manage employee compliance, conflicts of interest, personal account dealings, gifts and hospitality oversight, political contributions, external business activities, and information barrier controls through connected compliance technology.

As banks continue to overhaul their compliance infrastructures, technology's role has become a fundamental operational necessity for managing risk consistently across jurisdictions. Rather than supporting function, technology has become integrally embedded within the compliance landscape, underscoring the evolution from traditional models to more dynamic, interconnected systems in global banking.

08.06.2026

Karachi to get Billion Dollar Saudi-Backed Crypto and Smart Port Hub

Karachi's Waterfront Transformation: A New Frontier for Innovation and Trade

Karachi, Pakistan's bustling financial epicenter, is on the cusp of a transformative development. A significant stretch of port-owned land is poised to evolve into a vibrant hub of innovation, digital finance, and global commerce, thanks to a groundbreaking partnership between Pakistani and Saudi investors. This ambitious initiative is set to not only revolutionize the city's skyline but also redefine how Karachi engages with the global economy.

The Dynamics of the Partnership: A Synergy of Vision

The collaboration involves key stakeholders, including Saudi investors joining forces with notable Pakistani partners. Together, they aim to explore the creation of a sprawling cryptocurrency and blockchain zone in the thriving port city. This development will be complemented by a digital banking hub, smart port infrastructure, luxury real estate projects, and major healthcare and education facilities.

Memorandum of Understanding: Paving the Way Forward

The foundation of this groundbreaking initiative was laid with the signing of a memorandum of understanding (MoU) involving the Karachi Port Trust (KPT), the Saudi Business Council-Najd Gateway Holding Company, Arif Habib Dolmen REIT Management Limited, and the Pakistan Corporate Consortium. The MoU sets the stage for a collaboration that promises to bring unprecedented growth and development to Karachi's waterfront.

Project Scope: A Vision for a New Coastal Landscape

The proposed development encompasses approximately 140 acres of prime KPT-owned land on Moulvi Tamizuddin Khan Road. The plan is to transform this site into a modern commercial and maritime district that can attract regional and international investors. This ambitious project signals South Asia's increasing efforts to regulate digital assets and cryptocurrency trading, positioning Karachi as a nexus for financial innovation.

Comprehensive Urban Development: Blending Commerce with Technology

Plans for the area include a marine technology and logistics zone, smart port integration systems, digital customs services, and maritime software development projects. These initiatives aim to modernize Pakistan's shipping and port operations. Broadly, the vision incorporates international-standard hospitals, a medical university, a maritime and trade law school, luxury hotels, skyscrapers, corporate headquarters, and a large convention center.

Strategic Developments and Economic Potential

This announcement aligns with a recent visit by a Saudi delegation to Pakistan, where discussions also included potential ventures like an oil refinery at Gwadar Port and strategic oil storage facilities. The Karachi waterfront project is designed to fulfill all legal and regulatory requirements, aiming to attract investment, stimulate economic activity, and support urban renewal along the city's coastline.

Positioning Karachi in the Global Digital Finance Arena

The proposed crypto-focused district comes at a pivotal time when global competition for digital finance and blockchain investment is intensifying. Proponents believe this project could position Pakistan as a regional destination for technology-driven capital, strengthening ties with Gulf investors and fostering economic synergy.

The Rise of South Asia's Largest Integrated Waterfront Development

Should plans progress beyond the proposal stage, Karachi could soon witness one of South Asia's largest integrated waterfront developments. This mega project aims to combine cryptocurrency, digital banking, smart ports, energy, education, healthcare, and luxury real estate into a cohesive and prosperous urban environment.

05.06.2026

Four ways sophisticated swindlers are duping Canadians - and how to protect yourself

The Phone Call That Turned Bob McArthur's Life Upside Down

In March last year, Bob McArthur received a life-altering phone call that he believed to be from TD Visa. During the ensuing conversation, lasting four hours, the caller deceived Bob and his wife into believing their financial security was compromised. The couple was misled into surrendering their credit cards, only to discover later they had been scammed for nearly $14,000.

The Proliferation of Sophisticated Scams

Unfortunately, Bob McArthur's experience isn't isolated. Technology, augmented by artificial intelligence, has provided criminals with easier means to swindle unsuspecting individuals. The global and sophisticated structure of these scams is leaving governments scrambling to keep up.

The Emotional and Financial Toll on Victims

The weeks following the scam were filled with distress for the McArthurs as they attempted to navigate the fallout with their bank, which refused to cover their losses. The stress exacerbated Bob's health condition, inducing severe vertigo attacks and adding a layer of trauma to their ordeal.

Escalating Losses and Underreporting of Fraud

The rising tide of scams has resulted in significant financial losses for Canadian consumers, with reported fraud losses striking $704 million last year. However, this figure is believed to represent only a fraction of total scams, as victims often choose not to report due to embarrassment.

The Role of Technology in Modern Scams

Services that cater to scammers are easily accessible online, creating a thriving cybercrime ecosystem. AI facilitates the planning and execution of scams, while social engineering tactics have become an effective tool for tricking consumers into self-sabotage.

Investment Scams: The Lure of Easy Profits

Cases like Rick's, where he was drawn into fraudulent cryptocurrency platforms, highlight the predatory nature of investment scams. Despite initial returns, Rick was left in financial ruin, a scenario commonly faced by those lured into investment frauds with promises of high returns and urgency.

Psychological Manipulation and Economic Impact

Scams exert a powerful psychological grip, drawing parallels to compulsive gambling. Victims find themselves unable to admit defeat even as their losses mount, a psychological trap that reinforces their financial ruin.

Employment and Authority Impersonation Scams

Scammers are adept at impersonating authorities or employers, often compromising new employees by using their lack of familiarity to their advantage. These scams rely heavily on spoofing technology and detailed personal data to mislead victims.

Romance Scams and Emotional Exploitation

Romance scams leverage victims' emotional vulnerabilities, building false romantic connections that often lead to significant financial transfers. These scams often involve long-term emotional manipulation, which ensnares victims even after they realize the deceit.

Synthetic Identity Fraud

Fraudsters use synthetic identities to obtain credit under false pretenses. This type of fraud often combines legitimate personal details with fabricated information, impacting both businesses and individuals through unauthorized credit activities.

The Global Challenge of Tackling Scams

With the complexity and global scale of these fraud operations, effective solutions require a coordinated societal effort. Cross-industry and international collaboration, along with regulatory advancement, are crucial to combating this evolving threat.

A Path Forward for Prevention

Efforts like the Canadian Anti-Scam Coalition represent key steps towards tackling the scam epidemic. Consumer education, regulatory change, and shared industry responsibilities form the backbone of the long-term solution framework being developed to manage scam-related challenges.

Conclusion

As the tactics of scammers evolve, so must the defenses designed to combat them. This ongoing battle requires an adaptive and collaborative approach, ensuring that as one frontline against fraud is strengthened, new strategies are devised to counteract emerging threats.

Want to Be a Part of a New Trading World?

Simply provide us with your email, and our manager will contact you to get started.